TotalEnergies Germany Battery Projects Financing: The 3 Factors Behind 70% Debt

Four months ago, TotalEnergies signed a deal that most German battery developers cannot replicate. The company agreed to sell a 50% stake in 11 battery storage projects to Allianz Global Investors, structuring €500 million in total investment at 70% debt a use ratio that sits well above what the market typically accepts for merchant storage assets. The deal has circulated widely as "TotalEnergies secures $502m for battery projects in Germany," a figure that reflects a currency conversion of the same €500 million commitment, not a separate financing tranche.

The portfolio, developed by TotalEnergies subsidiary Kyon Energy, spans 789MW and 1,628MWh of capacity across Germany. All 11 projects are under construction and targeted for completion by 2028, according to the TotalEnergies press release. TotalEnergies will remain the operator.

This is not a signal that German battery storage finance has become straightforward. It is a proof point for a specific type of deal large, integrated, and timed with unusual precision against a closing regulatory window. Understanding why the debt share is possible here, and why it isn't for most developers, requires working through three things: revenue structure, regulatory timing, and sponsor quality.

Why the debt share matters for TotalEnergies Germany battery projects financing

70% debt on a battery storage portfolio is not typical. The market data explains why.

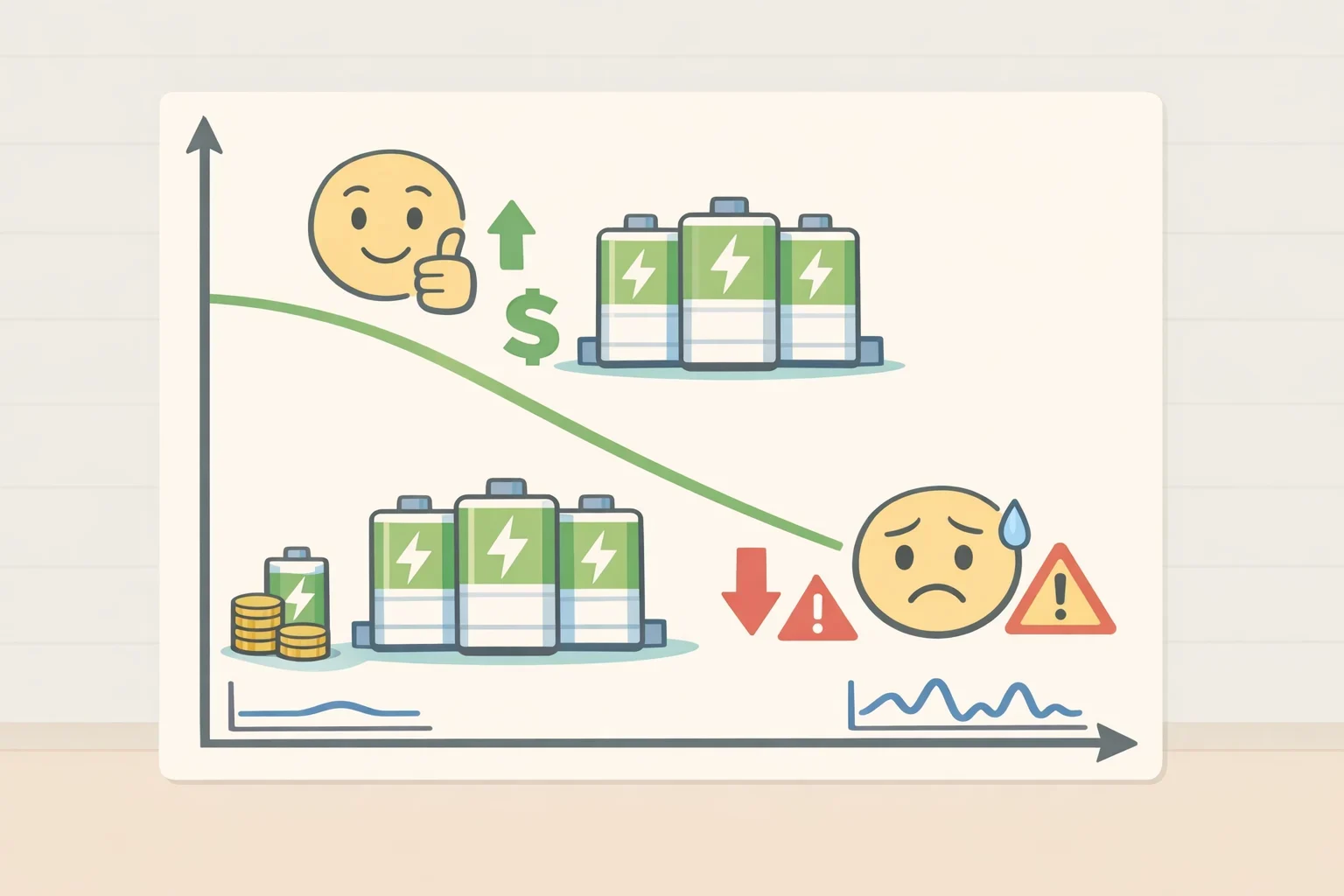

A battery operating on pure power market revenues earns roughly €115,000–130,000 per MW per year under central assumptions but that falls to around €70,000 per MW per year in a weak-market scenario, per Modo Energy's Q2 2026 German BESS outlook. That kind of range makes high use structurally difficult without some form of revenue floor. Lenders pricing a 20-year merchant exposure cannot assume the upside offsets the downside: a 50% drop in gas prices cuts day-ahead revenues by 37%, while an equivalent rise only lifts them by 28%.

Market saturation compounds the problem. A 50% increase in the German battery buildout would compress 2030 day-ahead revenues by a further 17%, Modo Energy found. Merchant exposure is therefore a two-variable problem gas prices and volume and neither variable moves symmetrically in the lender's favor.

Tolling structures address this directly. A full capacity toll locks returns at roughly 12% and can support up to 85% gearing by removing merchant exposure entirely. A partial toll blending a floor with residual market participation delivers 9–17% unlevered IRR across scenarios, holding the downside while preserving some upside, according to Modo Energy's analysis. TotalEnergies has not publicly disclosed its revenue arrangements for this portfolio, but Modo Energy's modeling suggests fully merchant batteries struggle to support this kind of use. Some form of revenue stabilization is what the debt ratio implies, even if the contracting structure hasn't been confirmed.

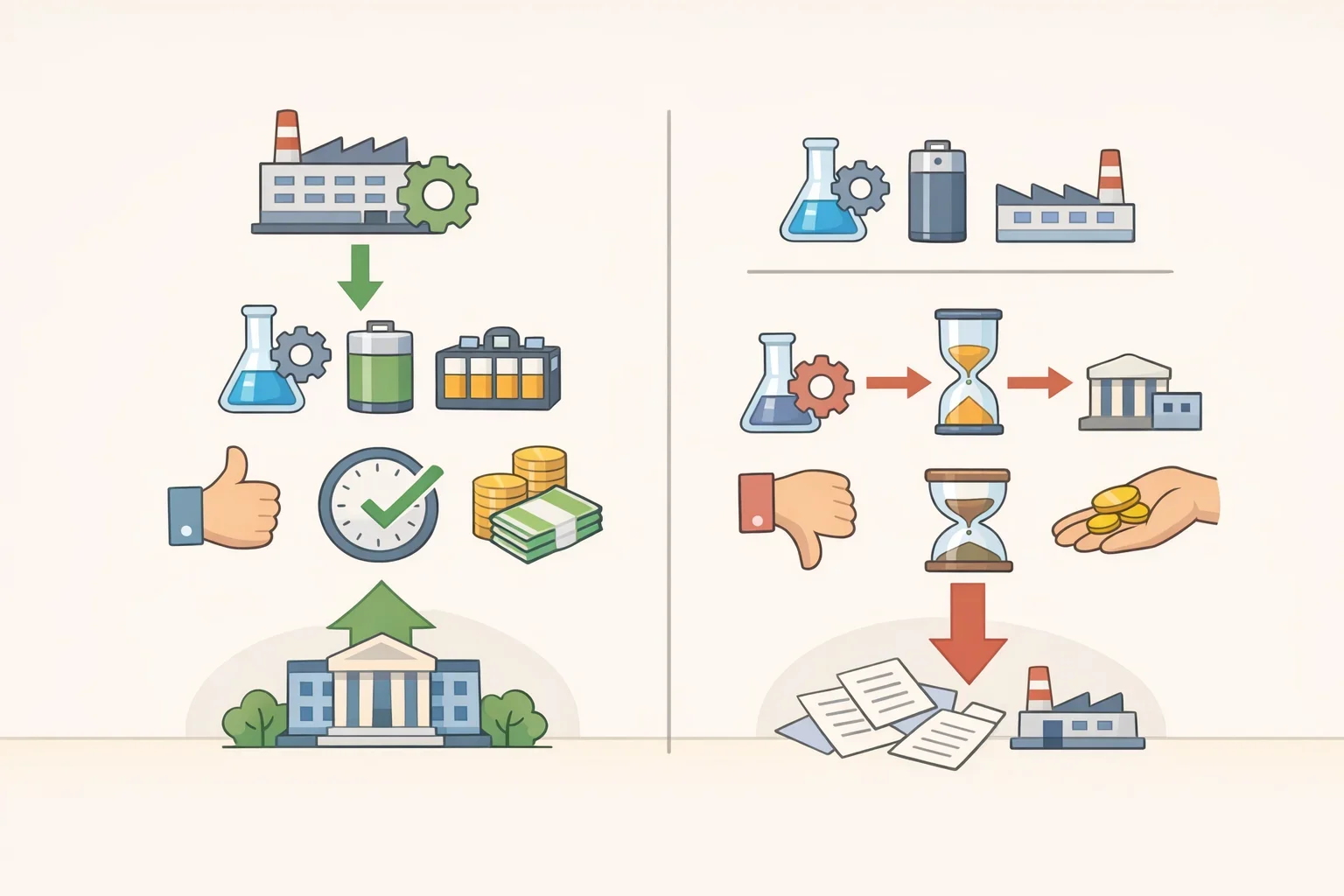

The supply chain picture adds a separate layer of lender comfort. Kyon Energy developed the projects, Saft another TotalEnergies subsidiary will supply batteries to most of them, and TotalEnergies will operate the assets throughout their life, per the press release. A pure-play financial developer cannot easily replicate that kind of vertical integration. Whether lenders formally priced it into their credit analysis is not disclosed, but having the developer, battery supplier, and operator all within the same group removes several of the execution risks that typically appear in project finance diligence.

How Germany's 2029 deadline shapes what gets financed

The regulatory backdrop is the second reason this deal looks different from most of what's in the German pipeline.

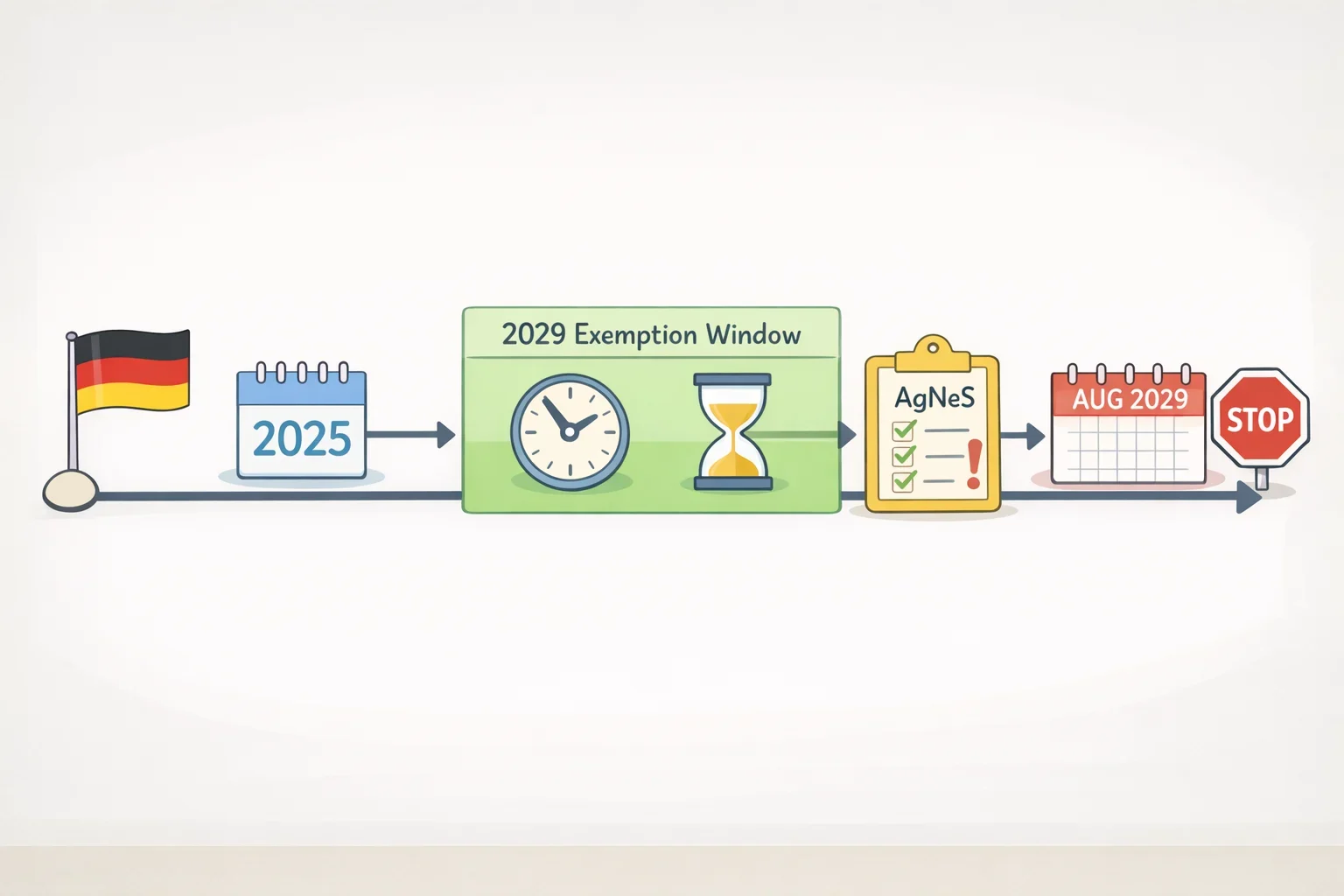

Under Section 118(6) of Germany's Energy Industry Act, battery systems commissioned before 4 August 2029 are exempt from grid charges for 20 years a provision that directly improves the revenue certainty lenders need to size debt, Energy-Storage.News reported last month. Projects that miss this cutoff face three new charge categories under the BNetzA regime instead, according to Modo Energy.

The financial cost of missing the window is not abstract. Unconstrained batteries can absorb roughly €20,000–25,000 per MW per year in charges before returns fall below hurdle rates but most new connections are flow-constrained, and those assets hit that threshold at just €10,000–15,000 per MW per year, Modo Energy's data shows. A moderate increase in charges under the new BNetzA regime could make many post-2029 projects unfinanceable at conventional use levels.

There is a further complication. Final grid charge values under the new regime may not be confirmed until late 2028, per Modo Energy. Lenders cannot size debt against a cost line they cannot model which is precisely why grandfathered exemption carries such financing value for projects that qualify.

The grandfathering protection has also grown more conditional. Under the current regulatory compromise, projects commissioned before August 2029 retain the exemption, but only if they can demonstrate a final investment decision before the AgNeS framework takes effect a deadline Germany's Federal Network Agency has placed around the turn of 2026/27, Energy-Storage.News reported. That FID threshold is not written into statute; it was introduced through the AgNeS process, layering procedural risk onto an already time-sensitive market.

TotalEnergies' portfolio was built to clear all of this. With 11 projects already under construction and targeted for 2028 completion, the portfolio sits well inside the 2029 commissioning threshold. That timing advantage over developers still in earlier pipeline stages is one of the deal's most straightforward structural edges.

What this means for developers beyond TotalEnergies

The transaction establishes a visible benchmark for what German battery storage financing looks like when conditions align and makes clear how demanding those conditions are.

Under central assumptions, German battery storage delivers 12–14% unlevered IRR; in the most adverse scenario, that falls to 5.5%, per Modo Energy. That range is wide enough to attract institutional capital when the downside can be managed, but it requires a revenue structure that most purely merchant projects don't currently have. The gap between headline return potential and financeable structure is where most deals stall. In 2025, only 40% of projected German battery capacity actually came online, Modo Energy data shows a reminder that pipeline announcements and operating assets are different things.

AllianzGI's participation signals that institutional appetite for the asset class is real. This marks Allianz's first direct equity commitment to a battery storage portfolio, per the press release. The constraint for the next wave of German battery projects is not whether investors are interested. It is whether developers can reach a demonstrable FID before the AgNeS framework closes the grandfathering window around the turn of 2026/27, Energy-Storage.News noted.

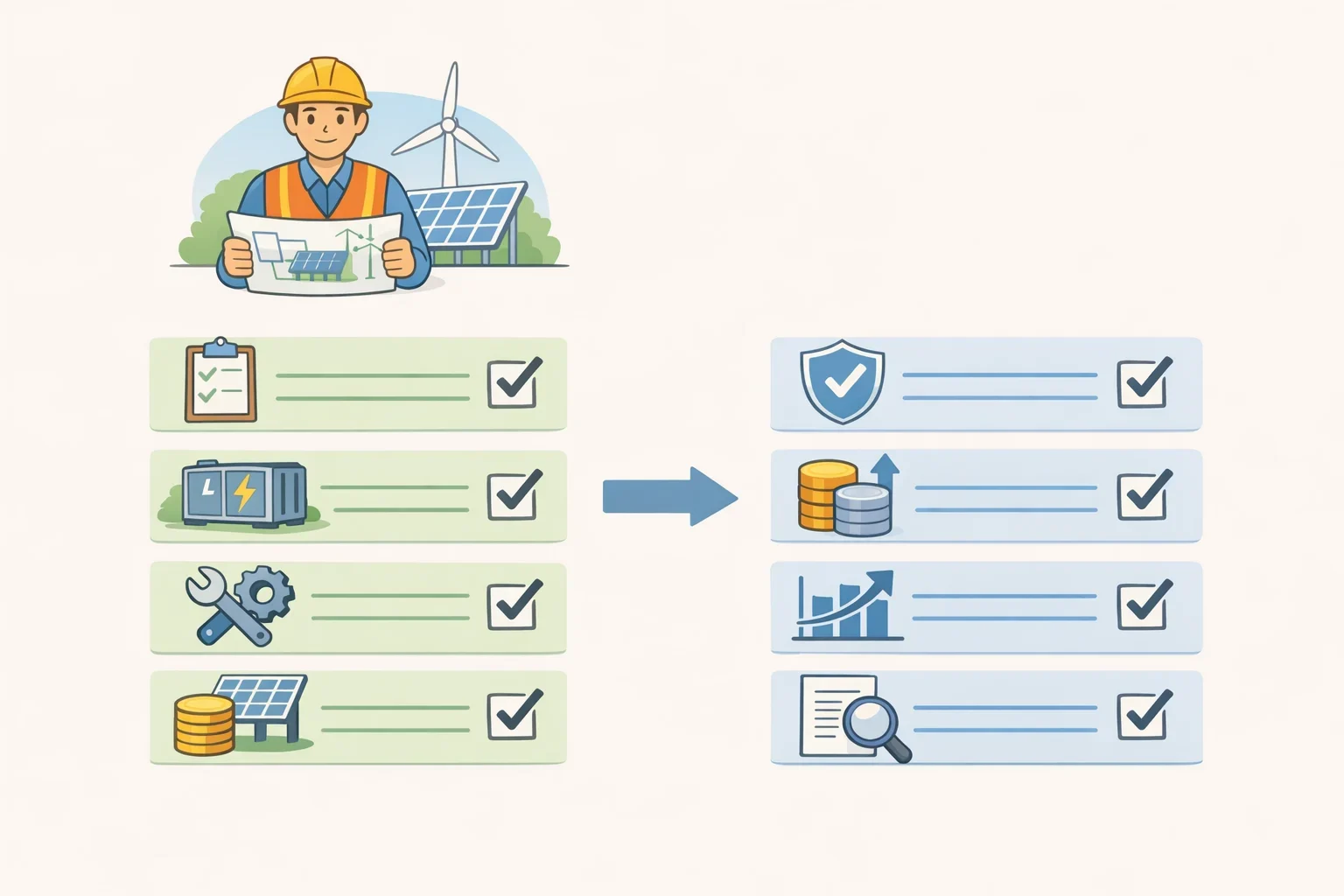

Taken together, Modo Energy's analysis points to four conditions that lenders are likely to prioritize when underwriting German battery storage at meaningful use: commissioning scheduled before August 2029; a demonstrable FID before AgNeS takes effect; some form of revenue stabilization toll, floor, or optimization contract sufficient to support debt service coverage; and either in-house or contracted delivery capability that reduces construction and supply risk. Projects that fall short on any of these are likely to find 70% gearing out of reach, and may find institutional equity terms harder to negotiate than what AllianzGI has accepted here.

The next test

The TotalEnergies–AllianzGI deal shows that German battery storage can be financed at institutional scale and at use ratios that make the economics work. It also shows that doing so required a combination of factors integration across the supply chain, revenue structure that controls the downside, and construction timing that locks in the 2029 exemption that came together in one portfolio at one moment.

The window for replicating those conditions is narrowing. The FID deadline under AgNeS is expected around the turn of 2026/27. The regulatory fee uncertainty runs through to late 2028. The merchant revenue outlook deteriorates if buildout accelerates.

The real test is whether a second wave of German battery projects from developers with less vertical integration and less timing advantage can attract comparable terms before those conditions shift. That is the market question this deal raises but cannot answer.