Databricks $188 billion valuation: what's behind the 40% jump in six months

Databricks has signed a term sheet for a new strategic funding round valuing the company at $188 billion, with existing investor Coatue Management leading what the Wall Street Journal reported as a $3 billion investment, expected to close later this summer, CNA reported today. Coatue declined to comment, and the $3 billion figure comes from Journal sourcing rather than a direct Databricks disclosure.

The Databricks $188 billion valuation sits $54 billion above the $134 billion mark the company carried in February, when it closed a $5 billion equity round alongside $2 billion in new debt capacity, CNBC reported five months ago. A 40% step-up in under six months is not typical, even in private AI markets.

One framing point before the numbers: this is a negotiated term-sheet mark, not a daily market-clearing price, and it is not directly comparable to a public market cap. Analysts widely see Databricks as a leading IPO candidate alongside OpenAI and Anthropic, per CNA, which means today's mark is also a signal of how private investors are pricing scaled AI infrastructure ahead of a public-market reckoning. Two things explain the gap between February and now. Revenue acceleration accounts for most of it. Private-market scarcity adds a layer of premium on top.

Why the Databricks $188 billion valuation jumped from February

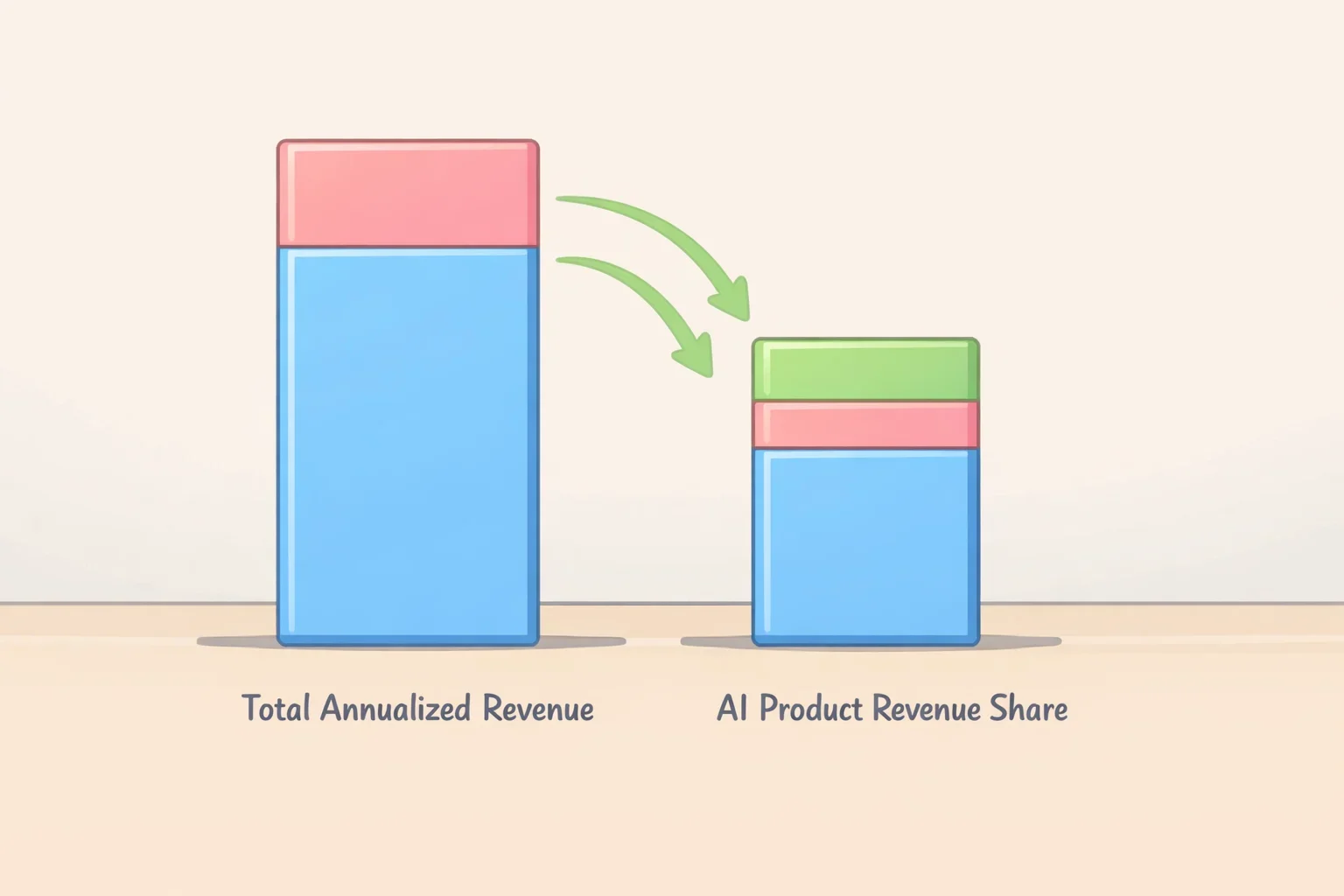

The numbers make this legible. At $6.9 billion in annualized revenue, a $188 billion valuation implies roughly 27x revenue. At $5.4 billion and $134 billion in February, the implied multiple was approximately 25x. The multiple ticked up only modestly; the larger driver is that $1.5 billion in additional annualized revenue materialized faster than the company said it would, CNBC reported last month. This is primarily a revenue event, not a multiple expansion story.

The clearest evidence is that Databricks outpaced its own guidance by a significant margin. In December 2025, the company forecast roughly 50% forward growth, per its press release. By February, annualized revenue was already at $5.4 billion with 65% year-over-year growth, CNBC reported five months ago. By June, the growth rate had climbed further, topping 80% on a $6.9 billion base, CNBC reported last month. Growth accelerated as the revenue base grew, which is the opposite of what scaling companies typically do. Beating a self-set forecast while doing it gave Databricks a straightforward rationale to ask investors for a higher mark.

The AI product line sharpens the picture. As of February, Databricks reported $1.4 billion in annualized AI product revenue, covering tools for building enterprise AI agents and applications on proprietary data, CNBC noted five months ago.

No updated figure has been confirmed today, but at the February run-rate that segment already represented roughly 26% of total annualized revenue. A product line at that scale and trajectory changes how investors model the medium-term revenue mix, and by extension what multiple they are prepared to pay for the whole platform.

One additional metric is worth flagging, with appropriate caution: net dollar retention above 140%, meaning existing customers have been expanding spend by more than 40% annually, according to Windsor Drake Research three months ago. That figure comes from an analyst report rather than a direct Databricks disclosure, so treat it as directional. What Databricks has confirmed directly, above-80% revenue growth, positive free cash flow, and $1.4 billion in AI product revenue, establishes the expansion case without relying on it.

What the Databricks strategic funding round says about private-market premiums

Even accounting for the revenue acceleration, a 27x revenue multiple on a private company warrants a structural explanation. Private marks for scaled AI-native companies have consistently run ahead of public-market revenue multiples, with Databricks the clearest example, Windsor Drake Research observed three months ago. Something beyond the operating metrics is being priced in.

That something is scarcity. The supply of independent, scaled AI-native data platforms is small enough that investors seeking exposure to enterprise data infrastructure at generative AI scale have very few places to put capital. No liquid alternative exists to arbitrage against, which lets motivated buyers tolerate a premium they would reject in a public market.

Illiquidity amplifies this in a specific way. Private investors do not face daily repricing against macro signals, competitor announcements, or quarterly misses. Valuation is set by negotiation on a slow cadence between parties who are both motivated to transact. The result is that private marks reflect not just current operating performance but the expectation of holding a scarce asset until an IPO creates a liquid exit, at which point the embedded premium could compress, hold, or expand depending on conditions at that time. The $188 billion is best read as fundamentals anchoring a floor and scarcity setting the ceiling, not as a claim about intrinsic value.

What has to stay true for the mark to hold

The current valuation rests on conditions that would need to hold simultaneously. Revenue growth staying well above 50% matters as an analytical benchmark: below that threshold, a 27x implied multiple becomes harder to support against public-market comps for high-growth software. If AI product revenue stalls as a share of total revenue, the rationale for pricing Databricks at a premium over traditional data infrastructure vendors would likely weaken. And if free cash flow turns negative, suggesting growth is being subsidized rather than generated, the multiple logic comes under pressure at any level.

That makes the next revenue disclosure the clearest near-term test. Watch whether annualized revenue crosses $8 billion while growth stays above 70%, whether the AI product revenue share climbs above its February baseline, and whether free cash flow remains positive. All three moving in the right direction would keep the current mark defensible. Any one softening significantly would pressure, in the liquid market, the premium that private investors have been willing to negotiate today.

CEO Ali Ghodsi has said the company will go public "when the time is right," per CNBC five months ago. With positive free cash flow and multiple large private raises in the past seven months, Databricks has no operational urgency to list on anyone else's schedule. The IPO prospectus, whenever it arrives, will be the first time public investors can apply audited full-year financials to a number private investors have now set at $188 billion. The growth trajectory it shows at filing is the real test of whether that figure was a starting point or a ceiling.