- Scribe Therapeutics IPO Files Without Clinical Trial Results

- What STX-1150 is and where the Scribe Therapeutics IPO stands scientifically

- How the 2026 IPO class compares and why the stage gap matters

- Backers, partners, and what Scribe is selling instead of data

- What the S-1 discloses and what investors must bridge on their own

Scribe Therapeutics IPO Files Without Clinical Trial Results

Scribe Therapeutics filed for a Nasdaq IPO on July 2, just weeks after dosing its first patient and with no clinical results in hand. The Scribe Therapeutics IPO, targeting the ticker "SCTX," arrives at a moment when every other biotech that reached public markets this year was already generating clinical data, Endpoints News reported. Most of those 13 companies were running mid-stage or Phase 3 trials when they filed. Scribe is weeks into its first human study.

The filing forces a specific question: can pedigree, partner validation, and a compelling platform narrative substitute for human proof when a CRISPR company targets a common cardiovascular condition rather than a rare disease?

What STX-1150 is and where the Scribe Therapeutics IPO stands scientifically

Scribe's lead program targets PCSK9, a protein with a well-established role in driving LDL cholesterol levels. STX-1150 uses a messenger RNA encoding an engineered CRISPR-CasX-based epigenetic silencer called ELXR, together with a guide RNA targeting PCSK9, delivered through lipid nanoparticles, per PharmaDeviceNews. The company argues that this approach damps down PCSK9 gene expression without altering the underlying DNA, which it says reduces the risk profile relative to permanent editing tools. That distinction is Scribe's framing, not an independently established fact.

Australian health regulators cleared the first-in-human study in May, Endpoints News reported. The Phase 1 trial is designed to enroll up to 64 adults with elevated LDL-C and heightened cardiovascular risk, evaluating safety, tolerability, and early biological activity, per PharmaDeviceNews. No human LDL-C lowering data exists yet.

Preclinical findings presented at the American Society of Gene and Cell Therapy meeting in May showed no off-target gene expression changes in tested conditions and no adverse findings in a GLP toxicology study. Manufacturing-scale STX-1150 also showed at least five-fold greater potency in primary human hepatocytes than in cynomolgus monkey cells, a result that supports the possibility of favorable human dose translation, PharmaDeviceNews noted. That potency gap matters: it suggests the drug may be effective at lower doses in humans than animal studies would predict, which has implications for both efficacy and the safety margin.

The commercial pitch is durability. A single infusion, Scribe argues, could replace PCSK9 inhibitors and other LDL-C treatments requiring daily pills, biweekly injections, or twice-yearly siRNA shots, Endpoints News reported. The adherence problem with chronic LDL-C therapies is real; the question is whether investors will price that opportunity before Scribe has shown its approach actually works in a patient.

Gene-editing companies have historically gone public on rare-disease programs, where small patient populations, high unmet need, and limited treatment alternatives make early clinical risk easier for investors to accept. A cardiovascular indication is a different proposition. The therapy will be weighed against decades of safety and efficacy data from statins, PCSK9 inhibitors, and siRNA therapies that already work reasonably well. That context is not unique to Scribe, but it does mean the evidentiary bar is higher and the absence of human data more consequential.

How the 2026 IPO class compares and why the stage gap matters

The 2026 biotech IPO class has not been forgiving of early-stage programs. All 13 companies that reached public markets before Scribe were already in clinical testing when they filed, including two of the largest biotech IPOs on record, Endpoints News reported. Most were running mid-stage or Phase 3 trials. That clinical bar reflects the selective conditions that allowed the IPO window to reopen after a difficult stretch; crossover investors funding pre-IPO rounds have generally insisted on seeing human data before putting capital into a story that will need to survive public market scrutiny.

Scribe's position is meaningfully different. The S-1 explicitly states the company has not completed any clinical trials, has no approved products, and acknowledges all programs carry a high risk of failure, per the filing. The IPO's practical necessity is not subtle: as of March 31, Scribe held $49.7 million in cash and marketable securities against an accumulated deficit of $175.1 million, the S-1 discloses. That runway is not long for a company at the start of a Phase 1 trial. The offering is a financing necessity dressed in a platform story.

Procedurally, the blank price range in the initial filing is standard for a first S-1 submission. The company must file at least one amendment before pricing, and that amended S-1 is where the actual terms appear. Until it lands, the IPO's valuation remains entirely open.

Backers, partners, and what Scribe is selling instead of data

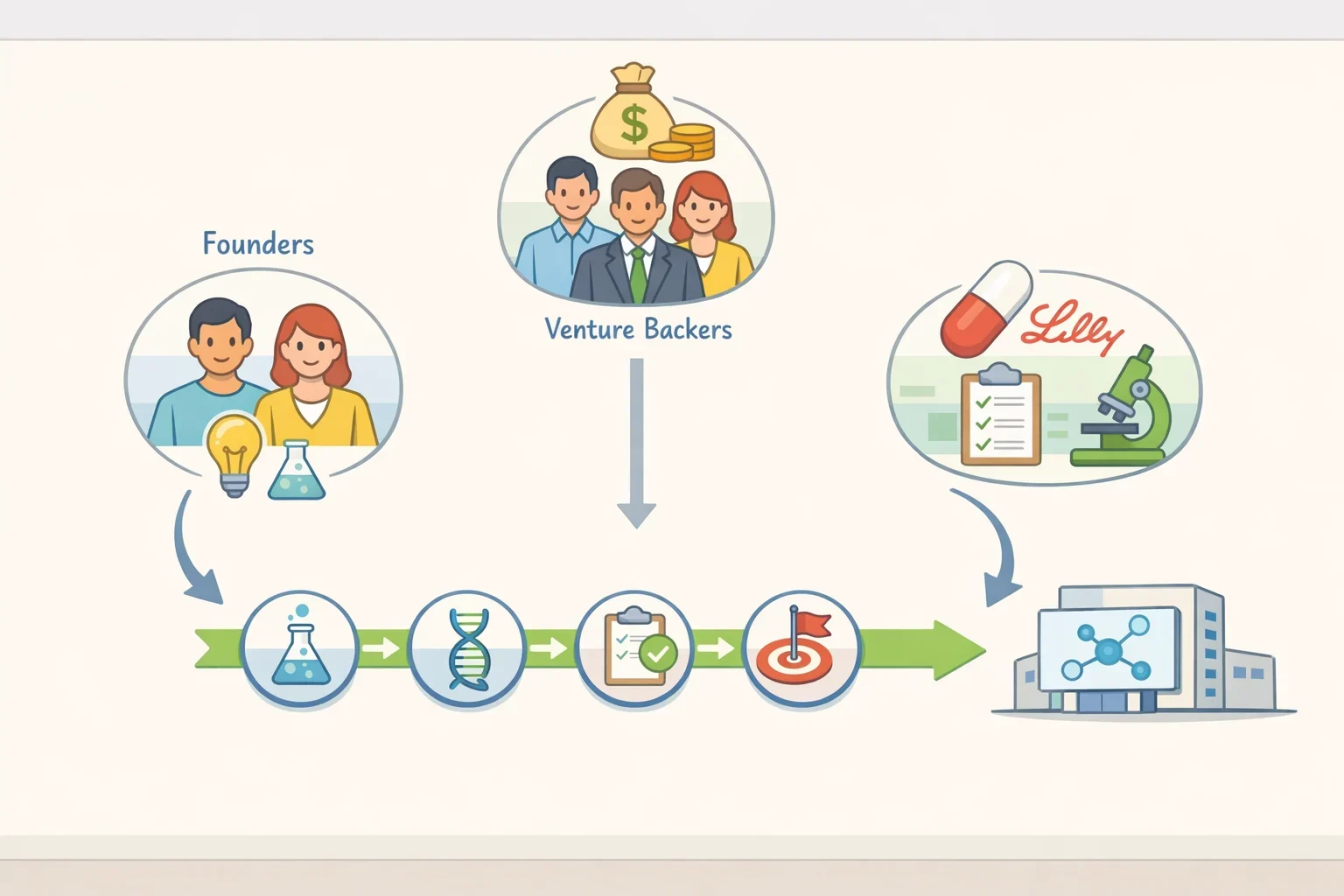

Scribe was founded in 2017 by CEO Benjamin Oakes and Nobel laureate Jennifer Doudna, who holds a stake exceeding 5% in the company. Andreessen Horowitz, Avoro Life Sciences Fund, and Eli Lilly also hold stakes above that threshold, per Endpoints News. The company has raised more than $150 million in private capital and, last month, disclosed more than $25 million in grants from the California Institute for Regenerative Medicine to advance two cardiometabolic candidates.

Lilly's position is worth examining on its own terms. The 2023 collaboration, which targets neurological and neuromuscular disorders using Scribe's XE gene-editing system, hit its second milestone in February. That deal makes Lilly simultaneously a cap-table stakeholder, a technology validator, and an active partner with skin in the outcome. Under the original agreement, Scribe is eligible for more than $1.5 billion in milestone payments across all programs plus low-double-digit royalties, according to a Scribe press release from earlier this year. None of that is revenue in hand, but the structure signals that a major pharmaceutical company has bet meaningfully on the platform.

The broader sector offers a reference point. Lilly paid roughly $1 billion upfront last year to acquire Verve Therapeutics' one-time gene-editing cardiovascular candidate, demonstrating that large pharmaceutical companies will price durable LDL-C approaches well before late-stage proof is in, Endpoints News reported. That transaction matters to Scribe's story because it shows strategic buyers have already established a valuation floor for the category, though the comparison is imperfect since Verve's candidate was further along when the deal closed.

Taken together, the founders, backers, and partner relationships form a credibility scaffold intended to support a valuation that no clinical data can yet anchor. The real question is whether public market investors, unlike concentrated crossover funds or strategic pharma partners with longer time horizons, will assign those signals the same weight.

What the S-1 discloses and what investors must bridge on their own

The filing is candid about Scribe's position. The company has never generated product revenue, expects to continue incurring losses for the foreseeable future, and warns that its stock will likely be highly volatile after listing, the S-1 states. None of that is unusual for early-stage biotech. The gap between where Scribe sits and where its 2026 IPO peers were when they filed is.

The investor belief set required here is fairly demanding. STX-1150 must demonstrate that epigenetic silencing of PCSK9 produces durable LDL-C reductions in humans, that the approach is safe enough for use in a preventive cardiovascular setting where regulators will compare it against therapies with decades of real-world tolerability data, and that a single infusion will eventually displace chronic treatments from a field with entrenched prescribing habits. Each of those is a reasonable hypothesis supported by preclinical evidence. None of them is proven.

The price range, total raise target, insider participation in the offering, and updated use-of-proceeds disclosures will all appear in the amended S-1. Those numbers are the most important facts currently missing from the story. They will show whether underwriters have priced in a premium for the platform pedigree and partner validation, or demanded a discount for the absence of human proof. That amended filing is when the market's actual answer to Scribe's IPO becomes legible. Until then, what Scribe has filed is a prospectus without a price which is to say, a compelling argument still waiting for its verdict.