David Beckham IM8 Funding: How General Catalyst's B CVF Deal Works

David Beckham's health drink startup IM8 has secured $1 billion from General Catalyst's Customer Value Fund, the company announced today. General Catalyst takes no equity and acquires no ownership stake in IM8. Instead, it receives a capped share of revenue from the customers the fund helps acquire, then exits the arrangement once it hits its return threshold, according to TechCrunch.

The David Beckham IM8 funding is only the second billion-dollar deployment from the CVF vehicle, and the structure is worth understanding on its own terms, independent of the celebrity co-founder attached to it.

How General Catalyst's Customer Value Fund works

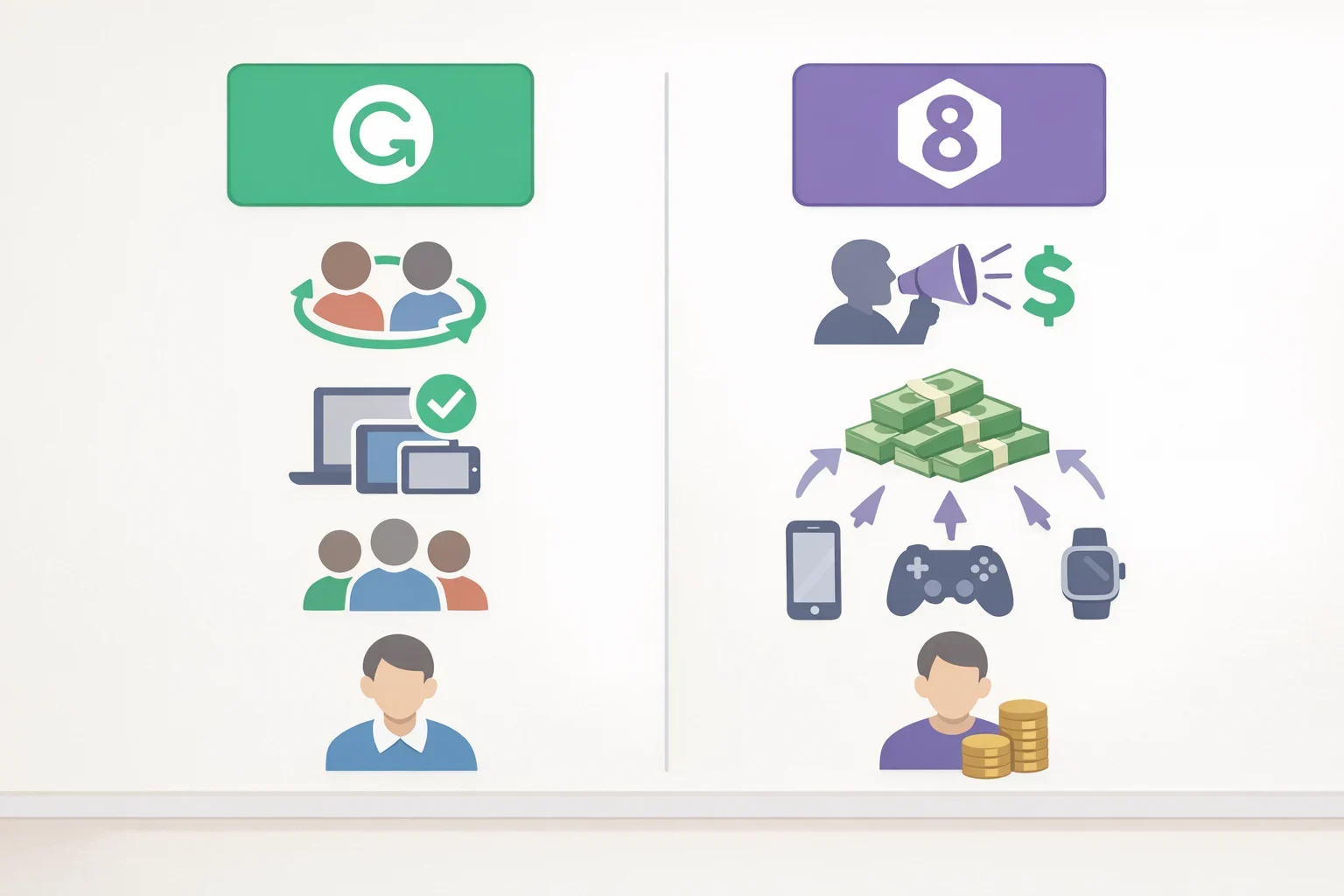

Standard venture rounds trade ownership for capital. The investor gets equity, the founder gets diluted, and returns depend on an eventual exit. Venture debt adds use but typically bundles in warrants and financial covenants that constrain how a company operates. The CVF does neither, per TechCrunch.

The fund issues what are essentially loans with non-standard repayment terms. Rather than repaying principal plus interest in the conventional sense, the borrower pays back the loan along with a fixed, capped percentage of revenue generated by customers the fund helped acquire. That revenue share is calculated as income from those CVF-acquired customers multiplied by a fixed gross-margin assumption, not actual realized margins, per TechCrunch. Once General Catalyst recovers its investment and hits its return cap on that "reference income," all subsequent revenue from those customers goes to Prenetics.

The capital is also targeted. The fund covers up to 70% of a portfolio company's customer acquisition costs, not general operating expenses or balance-sheet needs, per TechCrunch. That specificity is what makes the repayment mechanism coherent: General Catalyst finances customer acquisition, then collects a share of what those customers generate until it's made whole.

The structure has a defined finish line, which distinguishes it from open-ended equity dilution. Whether that finish line arrives cheaply or expensively for the borrower depends on two variables: how long the acquired customers stay, and how closely actual margins track the fixed assumption baked into the repayment formula. If real margins compress below that assumed figure, the effective cost of the capital rises. The formula doesn't adjust.

What the David Beckham IM8 funding shows about General Catalyst's CVF

General Catalyst has said the CVF suits companies with predictable revenue streams and a clear plan for how additional capital accelerates growth, per TechCrunch. Both criteria point toward subscription businesses. IM8 sells exclusively through subscription.

The product is a longevity-focused vitamin drink formulated with compounds including açaí fruit extract and Coenzyme Q10, per TechCrunch. Subscription customers commit to recurring purchases rather than one-off transactions, which means each acquired subscriber may generate a more predictable revenue stream over time. That kind of revenue profile is what the CVF's repayment structure is built around.

IM8 is a subsidiary of Prenetics, the health company that CEO Danny Yeung, a self-described high-school dropout, took public in 2022, per TechCrunch. A publicly listed parent structure may make underwriting more straightforward than it would be for an early-stage startup operating without public reporting obligations.

Companies that don't fit this profile share recognizable traits. Lumpy or unproven revenue makes the repayment structure difficult to model. Long CAC payback periods raise the cost of the capital before it has time to compound. Businesses still trying to establish their unit economics, hardware startups, pre-revenue biotech, marketplaces with variable take rates, can't easily offer the predictability the CVF repayment mechanism requires. The structure works when the economics are already legible, not as a tool for finding out whether they ever will be.

Grammarly, IM8, and a pattern worth noting

IM8 is only the second company to draw $1 billion from the CVF. Grammarly took the same amount in May 2025, shortly before acquiring email productivity app Superhuman, making IM8 the fund's second billion-dollar deployment in roughly 14 months, per TechCrunch.

The structural overlap is hard to miss. Both Grammarly and IM8 run subscription-driven revenue models. Both face significant customer acquisition costs as a central scaling challenge. Both had established operations before approaching the fund. The pattern suggests General Catalyst is building the CVF into a repeatable product for a specific type of company, not assembling bespoke arrangements case by case.

Two deals don't establish a trend, but they do define a thesis. The more interesting question the IM8 deal raises is one Grammarly doesn't directly answer. Grammarly serves business users; its customers tend to be sticky, with workflow integration that raises switching costs. IM8 is a consumer wellness subscription, where churn dynamics are structurally different. Subscribers may cancel when results feel uncertain, when budgets shift, or when a newer product enters the market. The CVF's fixed gross-margin assumption in its repayment formula doesn't account for that, and whether General Catalyst has priced the difference isn't clear from available reporting.

What to watch

Subscriber retention among CVF-acquired customers is the variable that will matter most as this deal matures. If those subscribers stay long enough, the revenue share clears its cap and the remaining lifetime value goes to Prenetics, potentially making the structure cheaper than a traditional equity round would have been. If they churn early, the repayment formula doesn't recalibrate downward.

General Catalyst has structured its return around a fixed margin assumption rather than actual performance. That protects the fund. The performance risk sits with Prenetics.

The "non-dilutive" label is accurate. General Catalyst holds no ownership stake in IM8, and the startup's ownership is not diluted, per TechCrunch. But non-dilutive is not the same as low-cost. The cost here is denominated in future revenue from specific customers rather than in ownership percentage, and founders evaluating similar structures should model that obligation against their actual retention and margin data before signing. How well IM8's subscribers stick is the figure that will tell the real story of this deal.