- Common Startup Fundraising Mistakes: Charles Hudson's Lessons From 500 Deals

- The benchmark has moved: what strong growth looks like to investors right now

- The overfunding trap: a bigger round is often the most consequential early-stage funding mistake founders make

- Common startup fundraising mistakes at pre-seed: what investors are reading when there's nothing else to read

- What to fix before optimizing the deck

Common Startup Fundraising Mistakes: Charles Hudson's Lessons From 500 Deals

Charles Hudson has invested in more than 500 startups, nearly all at pre-seed, nearly all before there was any conventional evidence the company would work. The common startup fundraising mistakes he keeps seeing aren't exotic. Founders walk into fundraising conversations misreading what they're being evaluated on. That single misread produces a predictable chain: a warped sense of how competitive their growth looks, a round sized to solve the wrong problem, and behavioral signals that close doors before a term sheet is ever realistic.

This week on TechCrunch's Build Mode podcast, Hudson spoke with Startup Battlefield lead Isabelle Johannessen about the headwinds facing early-stage founders and the errors most likely to kill a raise before it closes, as TechCrunch reported. Hudson is the founder and managing partner of Precursor Ventures, a firm built specifically to back founders before traction is apparent to anyone else. Before Precursor, he was a partner at SoftTech VC focused on mobile infrastructure which gives him a comparative vantage across more than one technology cycle, per TechCrunch.

Three threads run through his observations. The benchmark environment has shifted in a specific way that most founders haven't accounted for. That shift creates direct pressure to raise the wrong amount of money. And at pre-seed, the evaluation is already underway before the first slide, because there's no other evidence for investors to read.

The benchmark has moved: what strong growth looks like to investors right now

Venture capital has changed dramatically in the past few years, and founders who haven't updated their read on the current environment are likely to misread the feedback they receive, TechCrunch reported. The shift Hudson describes isn't incremental. Investors are no longer benchmarking a company only against its direct competitors or the prior year's funding cohort. They're comparing it against the fastest-growing AI companies in history a reference point that simply didn't exist for earlier startup generations.

The practical consequence is striking. Founders can double, triple, or quadruple their core metrics and still walk out of investor meetings hearing that the numbers look solid but not exceptional. Hudson put it plainly: "They're doubling, they're tripling, they're quadrupling, and the message they're hearing from the market is that's good but not great," as TechCrunch reported.

It's worth being precise about what this means. The problem isn't slow growth. The comparison set has expanded in a way that structurally disadvantages any company whose trajectory doesn't resemble an AI-native outlier. A non-AI founder with genuinely strong traction can now receive feedback that sounds like a soft pass and that feedback is accurate within the frame investors are using, even if it doesn't reflect the underlying quality of the business.

Hudson's read here is qualitative pattern recognition across hundreds of investments, not a calculated penalty backed by published data. But the experiential claim is specific: founders growing impressively by any prior standard are being measured against a new reference class, and most of them don't realize it until they're already getting confusing signals from the market.

That confusion tends to produce two predictable responses. Founders either interpret the feedback as a near-miss and keep pitching a story that isn't landing, or they overcorrect by chasing a larger round reasoning that a bigger number signals seriousness or buys credibility. Both moves go in the wrong direction. The second one, in particular, is where Hudson's sharpest warning applies.

The overfunding trap: a bigger round is often the most consequential early-stage funding mistake founders make

The standard founder logic here is intuitive: more capital means more runway, more time to find product-market fit, more buffer against the unexpected. Hudson's pushback isn't that this is wrong it's that the arithmetic ignores what a large raise does to strategic latitude, and that the consequences are asymmetric in a way founders almost never price in at the moment of signing.

"The real risk with these big rounds is you end up being a prisoner of your own company," Hudson said, as TechCrunch reported. "You raise all this money, and you've sold people on a big vision. They don't want the money back they want you to find a way to build something that's worthy of what they gave you."

The obligation an oversized raise creates is primarily strategic. Once a founder has sold investors on a large vision, every subsequent conversation circles back to a single question: is the company growing into the story that justified the check? That's a different and harder test than simply returning capital, and it persists through every board meeting, every milestone review, every future fundraise.

Consider two hypothetical early-stage startups this is an illustrative comparison, not a reported case. One raises conservatively and misses its 18-month milestones. The other raises aggressively and misses the same milestones. The first has room to adapt: a different product bet, a leaner team, a revised market thesis. The second has less of all three, plus an investor base anchored to the original story. Adaptation is possible in both cases, but the cost and friction of course-correcting are meaningfully higher after an oversized raise. That asymmetry is rarely on the table when the term sheet arrives.

The connection to the benchmark shift is direct, and it's where the trap closes. When founders feel their growth story isn't landing against investor expectations shaped by AI-era outliers, one instinctive response is to raise a larger round to signal ambition, compress the timeline, make the ask feel competitive. That's precisely when the logic is most dangerous. The round is solving a confidence problem. The business still has the operational problem, plus a new set of strategic obligations.

The obvious counterargument is real: undercapitalized companies lose to better-funded competitors, especially in fast-moving markets. Hudson's point isn't that capital is bad or that founders should deliberately constrain themselves. It's that round size should correspond to a concrete operational need, not to the story a founder believes they need to tell. A round sized to what the business actually requires over the next 18 months is a fundamentally different strategic position than one sized to absorb investor skepticism about growth benchmarks. They can produce identical pitch decks and very different outcomes.

The more useful starting point is to work backward from milestones, not forward from what the market might bear. What does the company need to prove in the next 18 months? What does proving it actually cost? That number not the maximum the founder thinks they can raise is the right anchor. Raising significantly beyond it doesn't buy flexibility. Over time, it quietly forecloses it, because the story that justified the larger check becomes the story the company is now obligated to execute.

Precursor was built to back founders before their traction was obvious, which means Hudson has watched what happens after oversized closes across a larger sample of early-stage companies than most investors encounter, per TechCrunch. The pattern he describes isn't a cautionary edge case. It's a recurring structural problem that the current benchmark environment is making more tempting to fall into.

Common startup fundraising mistakes at pre-seed: what investors are reading when there's nothing else to read

This is where calibration errors show up earliest and carry the most weight. At pre-seed, none of the conventional signals exist no revenue trajectory, no retention data, no customer acquisition cost, as TechCrunch noted. Investors aren't guessing in the absence of that data. They're redirecting their attention entirely toward what is present.

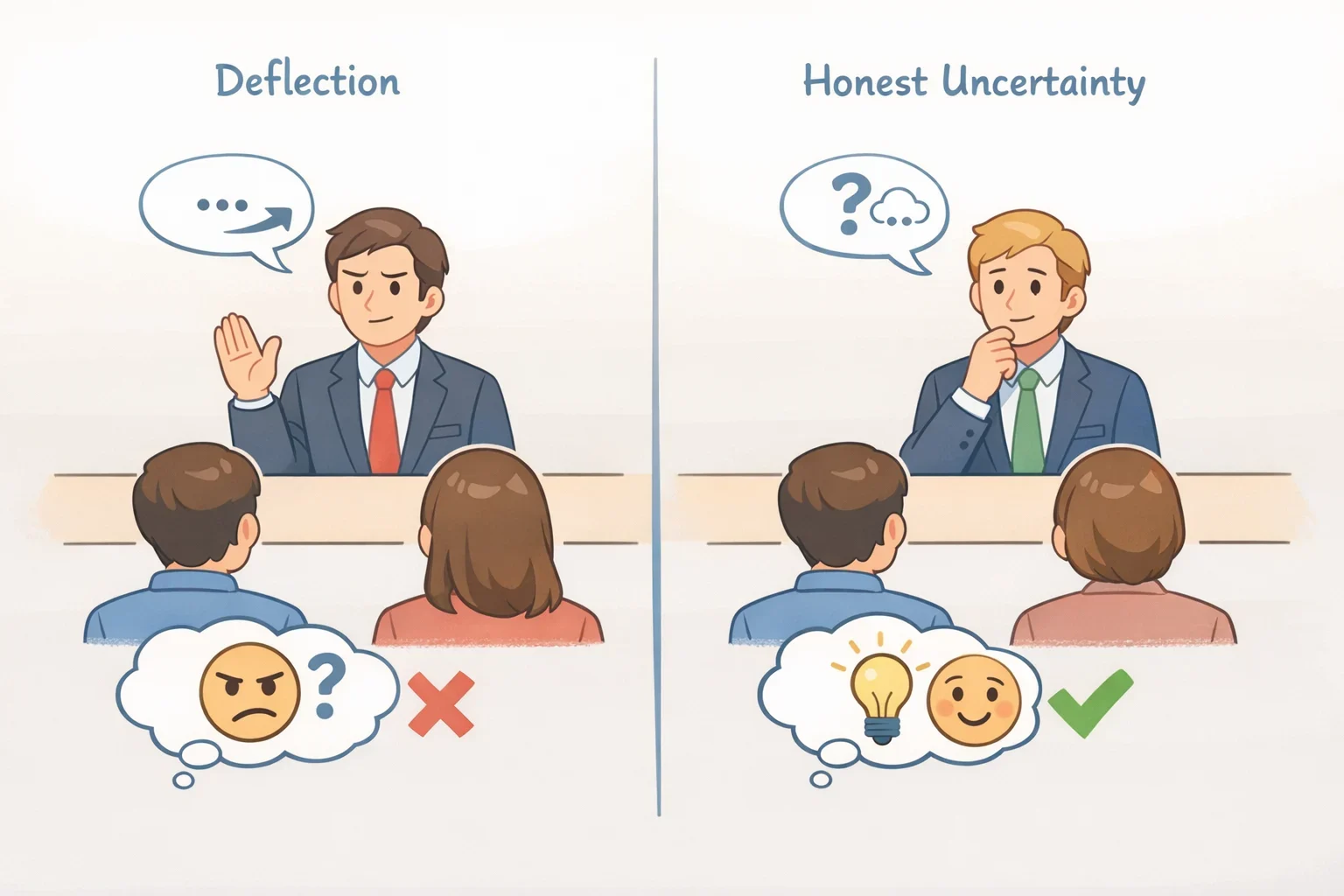

That's a meaningful distinction. It isn't that pre-seed investors are operating on gut feeling or goodwill. It's that the data they're collecting is different behavioral, qualitative, presentational and founders who treat the pitch as a data transfer are optimizing for the wrong test entirely.

Hudson has been specific about how founders underestimate the weight of choices that appear minor: how they respond to hard questions, what they choose to emphasize, how they handle uncertainty when a line of questioning doesn't go where they expected, per TechCrunch. Those signals can end a conversation before a term sheet is ever a realistic possibility. The source material confirms that Hudson identifies specific red flags at this stage and that certain behavioral patterns reliably spook investors early though a complete enumeration isn't available. What it does confirm is the category: when everything else is speculative, the signals that aren't speculative carry disproportionate weight.

The gap between what founders think they're being evaluated on and what investors are actually watching is probably widest here. A founder who spends weeks perfecting a financial model for a company with no revenue is solving for the wrong problem. What an experienced pre-seed investor is actually reading is whether the founder understands their own blind spots, handles uncertainty honestly, and demonstrates the kind of judgment that suggests they'll make sound decisions with someone else's capital. Those aren't soft criteria or secondary concerns. They're the only reliable proxy available at a stage when everything else is, by definition, speculative.

There's a specific texture to honest uncertainty that experienced pre-seed investors recognize. A founder who fields a hard question with a confident non-answer pivoting to a talking point, deflecting with enthusiasm signals something different than a founder who says "that's the hardest part of this, and here's how we're thinking about it." The second response might feel riskier in the room. It tends to land better with investors who've sat across from hundreds of founders and learned to read the difference.

This dynamic shifts meaningfully at seed, where some financial signals do exist and the conversation moves toward growth rate and unit economics. At pre-seed, the founder is the product demonstration. How the conversation goes is the primary data point an investor has. Preparing for hard questions and being honest rather than polished in response to them is at least as valuable as a well-constructed deck. For many investors at this stage, it's more valuable.

Hudson built Precursor specifically to back founders before their traction was obvious, which means his evaluative instincts at the pre-seed stage have been tested across a larger sample of pre-obvious companies than most VCs encounter, per TechCrunch. That sample shapes the pattern recognition in ways that matter precisely because the metrics don't exist yet.

What to fix before optimizing the deck

Across Hudson's observations, one diagnostic question does more work than most pitch preparation: what is this investor actually measuring right now, given this stage and this market?

At pre-seed, the answer is judgment and behavior, because nothing else is available. Preparation that focuses on handling uncertainty honestly rather than projecting confidence is more likely to land. At seed and beyond, the question expands to include growth metrics and those metrics are now being measured against a comparison set that includes AI-native companies growing at rates most founders' models don't account for.

On round size, the question is whether the capital requested corresponds to a concrete operational milestone or to a vision designed to make the ask feel competitive. The two can look nearly identical in a pitch deck. They produce very different outcomes after the close, because one of them creates obligations the business isn't yet positioned to meet.

Hudson's view reflects one firm's philosophy and won't map exactly onto every fund's criteria. Precursor is deliberately pre-obvious, high-risk, founder-first a specific posture that shapes everything Hudson looks for. But the core observation travels beyond that posture: the most common early-stage fundraising mistakes are calibration mistakes. Founders are solving for the wrong variables, optimizing for signals investors aren't reading, and sizing rounds against a confidence problem rather than an operational one.

Fix the map first. The pitch prep problem gets easier from there and so does every conversation that follows it.