- Amazon Multi-Tranche Bond Offering Explained: Inside the 2026 AI Debt Strategy

- Amazon bond offering 2026: what changed between March and June

- What the filings say versus what market reporting suggests

- The strategic reversal: from paying down debt to depending on it

- Why markets kept the window open

- What to watch next

Amazon Multi-Tranche Bond Offering Explained: Inside the 2026 AI Debt Strategy

In March, Amazon closed the largest corporate bond sale in history. Four months later, it assembled another $31.5 billion in financing inside 48 hours. Taken together, the Amazon multi-tranche bond offering and subsequent bank loan represent something more durable than opportunistic borrowing: a company whose AI spending program is expected to push free cash flow into negative territory, forcing it to treat debt markets as a permanent funding source rather than an occasional one.

Bond investors are the audience most directly exposed to what happens next.

Amazon bond offering 2026: what changed between March and June

Amazon's financing campaign this year runs in two distinct phases, and conflating them obscures what each one reveals.

The first phase closed in March. Amazon priced $36.898 billion in senior unsecured USD notes across 11 tranches, per the company's prospectus supplement filed with the SEC. The structure mixed floating-rate paper tied to Compounded SOFR with fixed coupons running from 3.850% on the two-year notes to 6.050% on the 50-year. Net proceeds came to approximately $36.813 billion after underwriting discounts, per Amazon's 8-K filing. That USD deal priced alongside a €14.5 billion euro offering, Amazon's debut in that currency, bringing the combined total to $53.8 billion-equivalent across 19 tranches. The previous record, Verizon's $49 billion deal from 2013, had stood for over a decade, IFR reported.

The second phase arrived last month. Amazon raised $14 billion through a Canadian-dollar bond sale, rated AA- by Fitch on the proposed notes. Within 48 hours, it followed that with a $17.5 billion three-year senior unsecured delayed draw term loan arranged by a syndicate including JPMorgan Chase, Citigroup, Wells Fargo, HSBC, and BofA Securities, according to TechCrunch citing Bloomberg.

The loan structure is worth a moment. Unlike a standard term loan where the full amount arrives at closing, a delayed draw facility lets Amazon pull capital on its own timeline. Commitments expire September 30, 2026 unless fully drawn beforehand, Fitch noted. That draw flexibility, paired with bond maturities stretching to 2076, points to a management team that expects the AI spending cycle to run for years and wants a capital structure to match: patient on timing, long on duration.

What the filings say versus what market reporting suggests

Company disclosures and outside reporting tell related but different stories on where the money goes.

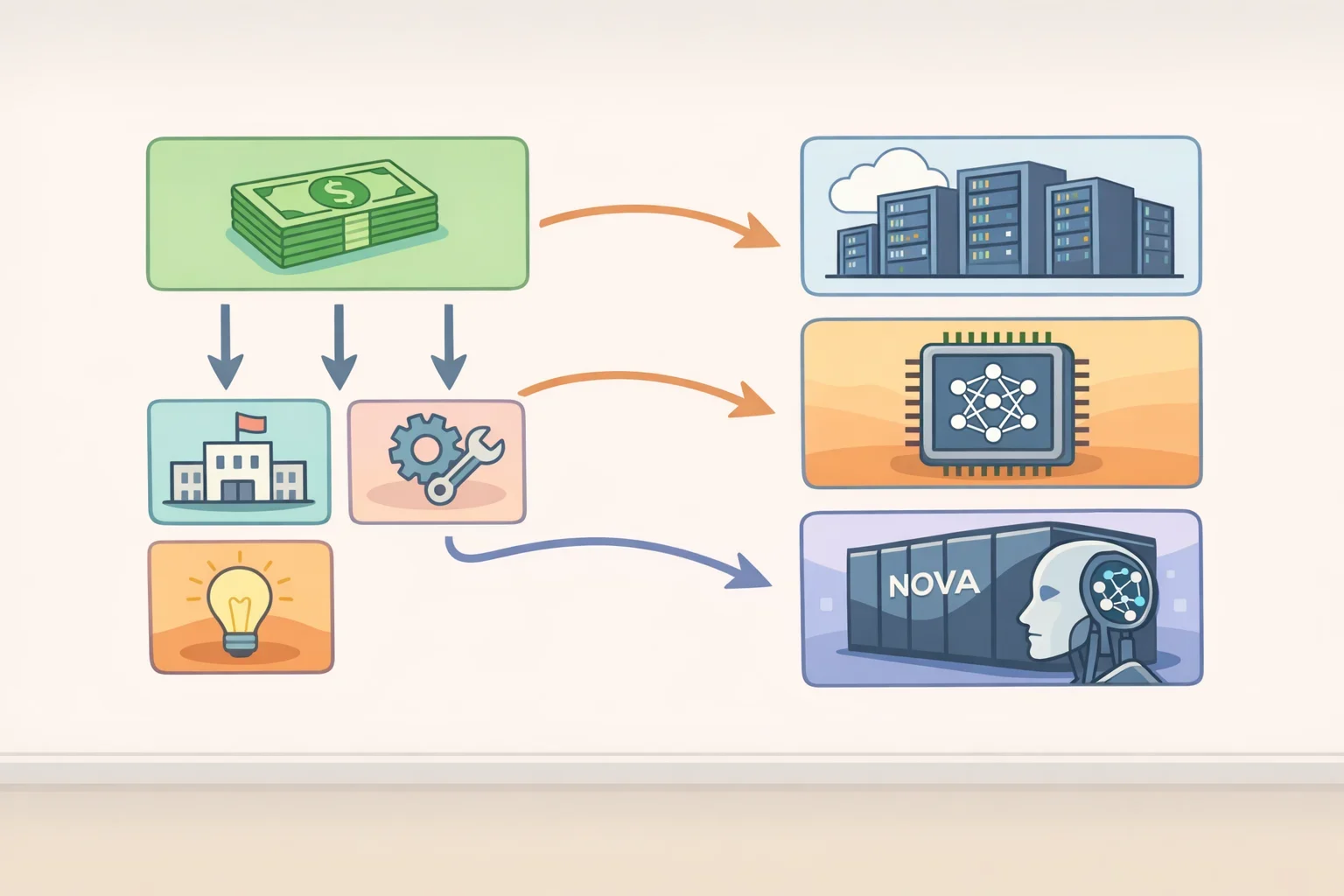

Amazon's prospectus lists intended uses for the USD notes as general corporate purposes, explicitly defined to potentially include debt repayment, acquisitions, investments, working capital, investments in subsidiaries, capital expenditures, and share buybacks. Fitch narrows the framing somewhat for the Canadian notes, flagging increased capex and strategic investments as the earmarked purpose. All of the new paper, bonds and bank loan alike, is senior unsecured and ranks equally with Amazon's existing senior debt.

The market-level context comes from IFR, which reported in March that Amazon plans to spend $200 billion this year building data centers, developing custom chips, and training its Nova AI model, more than any of its hyperscaler peers and the largest single-year corporate investment program ever seen. IFR also reported on a potential investment of up to $50 billion in OpenAI, though that figure comes from market reporting rather than company disclosures and should be read as unconfirmed context, not a confirmed use of bond proceeds.

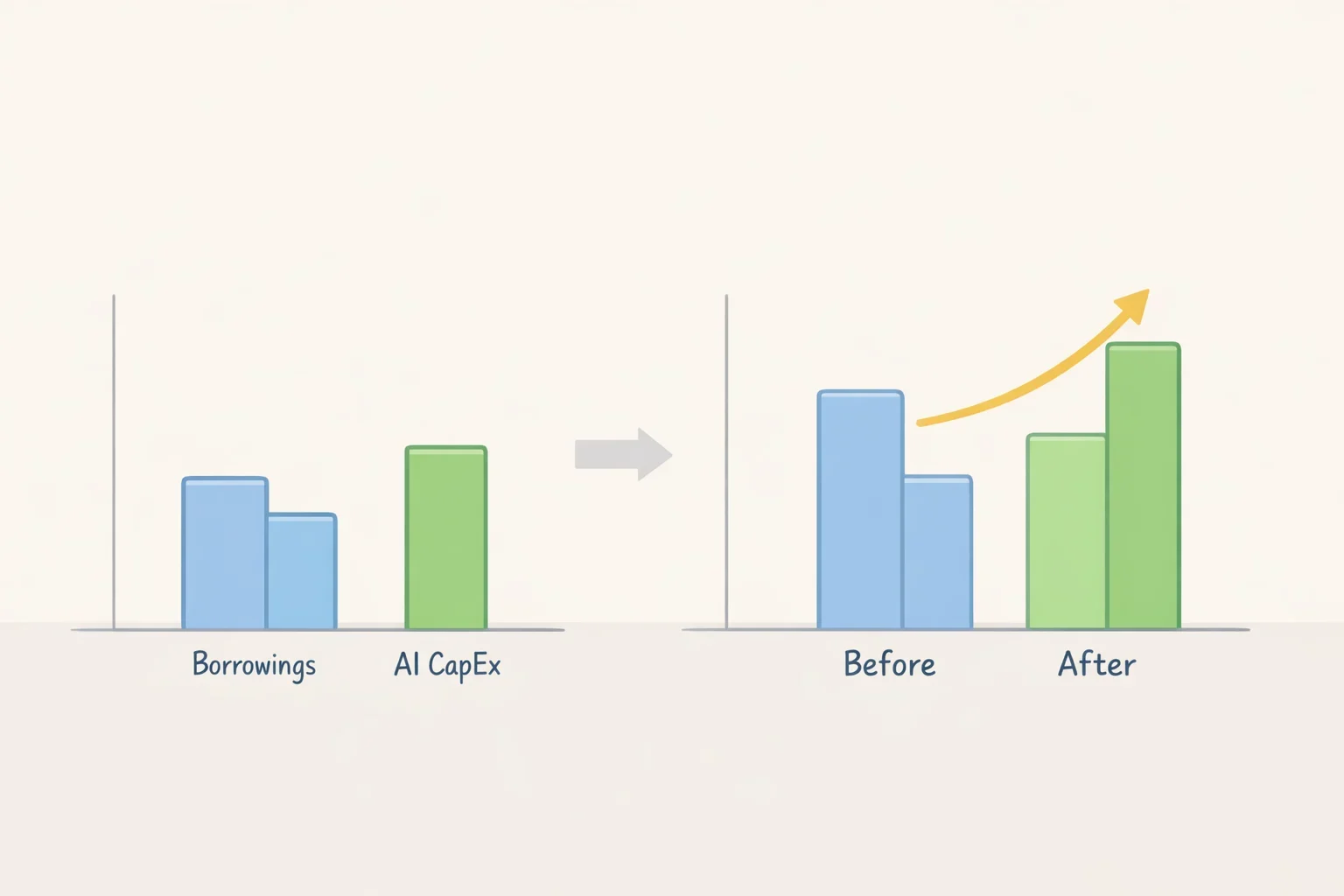

The spending program is set to push Amazon's free cash flow into negative territory, IFR reported. That is the clearest explanation for why the debt raises are structural rather than tactical. A company running negative free cash flow cannot fund a $200 billion capex program from operations alone.

The strategic reversal: from paying down debt to depending on it

The shift in Amazon's balance sheet is sharp enough to be worth stating plainly. Total borrowings rose to approximately $122 billion following the March deal, up from roughly $58 billion as of late October 2025, IFR reported. That is not gradual use creep. Borrowings roughly doubled in under five months.

For years after its 2010s expansion, Amazon paid down debt as free cash flow strengthened. AI has changed the math entirely. The four largest publicly listed hyperscalers, Alphabet, Amazon, Meta, and Microsoft, are collectively expected to spend $630 billion on capital expenditure this year, about 50% more than last year, IFR reported. Amazon is the highest individual spender in that group, and internal cash generation cannot keep pace with that rate of deployment.

Issuing across multiple currencies, at tenors stretching to 2076, and layering in a bank facility with flexible draw timing reflects a working assumption that the AI investment cycle will run for years, not quarters. Bonds maturing in 2066 and 2076 are not a bridge to something else. They are a bet that the economics of AI infrastructure will justify the use eventually, even if not soon. That is a long time horizon expressed through liability management.

Why markets kept the window open

Amazon's March record deal did not price into a calm environment. Middle East conflict had driven oil prices up roughly 30% and effectively shut the primary U.S. bond market the prior trading day, IFR reported. Amazon went anyway. The deal drew approximately $158 billion-equivalent in orders across both legs, nearly three times the final deal size.

JPMorgan's global co-head of investment-grade debt capital markets, John Servidea, put the demand in direct terms: "Notwithstanding just how volatile markets are right now, for the right companies, the truly great companies and credit stories, there is still a tremendous amount of capital available," IFR quoted him as saying.

Fitch's AA- rating on the Canadian notes, consistent with Amazon's existing debt ratings, signals the agency views the use increase as manageable at this stage. The senior unsecured structure across all new paper keeps the obligations straightforward for buyers and maintains balance-sheet simplicity.

The capacity question is worth watching at the sector level. IFR estimated total hyperscaler bond issuance in 2026 could reach $400 billion across the industry. At some point, even strong demand for highly rated names has limits, particularly if the AI revenue thesis becomes harder to substantiate with near-term numbers.

What to watch next

Three signals will clarify how this financing story develops from here.

1. Whether Amazon draws the DDTL before September 30. The $17.5 billion delayed draw facility expires at end of September unless fully drawn beforehand, per Fitch. A full draw indicates AI deployment is on schedule and that Amazon has specific capital needs lined up. A partial draw or expiry raises questions about timing slippage in the buildout, or whether other financing has moved ahead of it in the queue.

2. Whether ratings agencies hold the current floor. Borrowings have roughly doubled since late October 2025, reaching approximately $122 billion, IFR reported. If free cash flow turns negative, credit metrics will come under pressure. A downgrade or negative outlook from Fitch or its peers would raise Amazon's cost of debt and constrain issuance volumes. Stability, by contrast, confirms that the market accepts Amazon's long-term investment logic.

3. Whether Amazon returns to the bond market before year-end. The shelf registration filed in February 2026 gives ongoing issuance capacity, per Amazon's 8-K filing. A return, particularly in a new currency or at ultra-long tenors, would confirm that debt has become a routine funding tool for the AI buildout rather than a response to a specific near-term capital need.

The first of those answers arrives by October.