Tax deductions from gross wages pare down the size of a paycheck and may leave employees wondering how they will ever be able to save for retirement. However, thanks to pretax retirement contributions allowed by the IRS, both employers and their employees can save on Social Security and other tax payments every payroll period.

A contribution is the amount of money that either an employee or the employer pays into a retirement account. Employer-sponsored plans typically allow employees to elect to have a portion of their gross earnings deducted from their pay and placed into the retirement plan before any taxes are calculated.

Examples of this type of plan are the 401(k), 403(b) and the SIMPLE IRA.

Each plan has its own specific rules, and the IRS issues a standard limit on the total amount that may be contributed annually. The limit for 2018 is $18,500 or up to 100 percent of the employee's compensation, whichever is less.

Participants over age 50 are allowed to contribute an additional $6,000.

Elective deferral contributions save everyone on the tax amounts owed when it comes to calculating payroll deductions for Social Security. The contributions are allowed pretax, so the amount is first deducted from gross earnings and therefore is not used in the calculation of Social Security.

Keep in mind that these funds will be deemed as income and taxes will apply when the funds are withdrawn upon retirement.

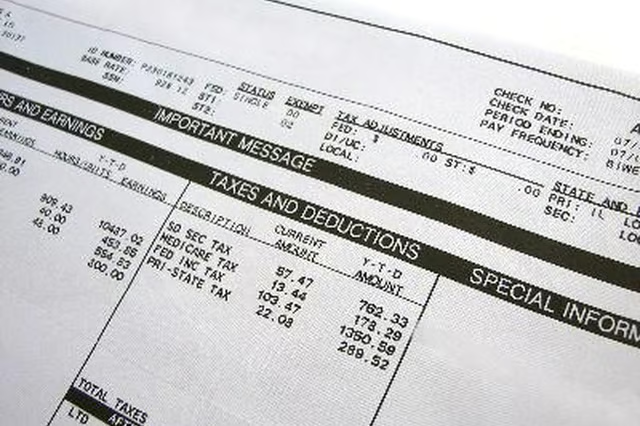

After retirement contributions are deducted, the Social Security tax, currently at 6.2 percent for both employees and employers, is then calculated based on the remaining amount. It is then deducted from the employee's pay.

For someone earning $3,000 biweekly and contributing $300 to a 401(k) each pay period, the taxable earnings are reduced to $2,700. The result is a tax savings of $18.60 each pay period. That may not seem like much, but nearly $500 a year stays in an employee's pocket.

Employers also save with pretax contributions. Since businesses are responsible for paying a matching portion of their employees' Social Security, the same tax savings are passed on to employers. This amount can represent considerable savings when you consider all the participating employees in the company.

When considering which plans to offer your employees, take into account that Roth IRA contributions are not tax-deferred. That means that taxes, including Social Security, are calculated on the full amount of gross earnings, so there are no tax savings up front with this retirement savings option.

However, Roth IRAs benefit employees in that those funds are not taxed upon withdrawal at retirement. In this way, employees can balance their retirement savings tax burden between funds by paying some taxes while they still work and some at retirement.