Corporate tax returns appear in the same format as other financial data, making it difficult for uninformed readers to comprehend the information. Corporate tax returns are comprised of a variety of financial and informational data. Understanding the tax return helps you assess the financial condition of a corporation, in addition to its size, affiliations and ownership.

Things You Will Need

IRS form 1120 income tax return

IRS form 1120 instructions

Review the information sections of your form 1120 income tax return, familiarizing yourself with pertinent information about the corporation. The top information section on the first page of form 1120 contains a summary of basic information about the corporation. The remainder of page one through line 31 is equivalent to the profit and loss, or income statement. You will address this data after reviewing the remaining information sections.

Locate schedule K by turning to the third page of form 1120. Schedule K displays other information, including the accounting method, which profoundly affects the results of the financial statements. The middle sections of schedule K address the business activity codes and control and affiliation groups. Questions 6 through 13 of schedule K provide the IRS with additional reporting information used to determine additional reporting requirements.

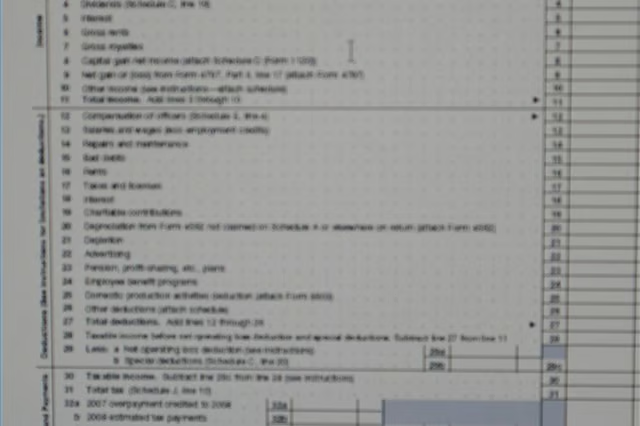

Move to the first page of form 1120 and review the income section contained in lines 1 through 11. The income section includes gross income less returns and allowances. Gross income is the primary income source for the corporation. Cost of goods sold follows gross income and is the cost of any products acquired and sold during the accounting period. The net of gross income less cost of goods sold is the gross profit. Lines 4 through 10 display other income totals, delivering total income on line 11.

Determine the deductions, or expenses, incurred by the corporation. The second section of page one on form 1120 includes selling, general and administrative expenses, or SG&A. Selling expenses directly relate to sales and include sales salaries and wages, advertising, sales meals and entertainment and supplies. General and administrative expenses indirectly relate to sales and include expenses such as rent, repairs and maintenance, non-sales salaries, interest and depreciation. Expenses not listed in one of the categories in lines 12 through 25 appear on a statement, totaled on line 27 as other deductions. Total deductions net against total income and result in taxable income on line 30. Line 31 displays the corresponding total income tax for the corporation, followed by credits, payments and amounts owed or refunds. Balances on line 34 indicate an amount owed, while balances on line 35 indicate an overpayment.

Turning to the second page, you see schedule A, which displays the components of your cost of goods shown on line 2 of the first page. Determine the inventory reporting method from the displayed information at the bottom of schedule A. Dividends and special deductions report as components of equity, not as deductions from income. Schedule E is a detail of office compensation paid, summarized in the first page of form 1120 on line 12. The Internal Revenue Service requires corporations to report this information. Schedule J provides details on the computation of income tax for the corporation.

Review the corporation's prior and current year balance sheet in schedule L, which is comprised of assets, liabilities and equity. Schedule L begins with current assets, including cash and accounts receivable, and progresses to less liquid assets, finishing with fixed, intangible and other assets. Liabilities appear in the order they are due, and include accounts payable, other current liabilities and other liabilities. Equity follows liabilities and includes capital stock, additional paid in capital, retained earnings and treasury stock. Schedule M-1 reconciles the corporate tax return to the corporation's books and schedule M-2 reconciles retained earnings. For additional assistance deciphering information on a corporate tax return, contact your local enrolled agent, and tax specialist licensed by the Department of the Treasury.

Tip

Always review the accounting method before previewing the income statement or balance sheet data

Make sure you are reading a form 1120; there are several other corporate tax return forms.

Warning

Total assets of less than $250,000 on page 1 allow the corporation to not report schedule L, or the balance sheet or schedule M-1 on page 5.

Tax and financial accounting are not the same; you may find discrepancies between a corporate tax return and the corporation's books.